Building Financial Literacy

How understanding your ‘Money Story’ sets a solid foundation for improving your money habits

Image courtesy of Kailanianna (Kai) Ablog

When people discuss financial literacy, they often talk about budgeting, taxes, and investing in the stock market. While these are helpful, not many bring up an essential part of building fiscal confidence: understanding how money can influence your life, actions, and decisions.

The Tip of the (Money) Iceberg: What is Financial Literacy?

If you have spent time diving into the world of money, you may have been berated with a plethora of terms and abbreviations that, at first glance, make little to no sense: index funds, Roth IRAs, tax code, 401(K)s, etc. If these “word salads” intimidated you and made you go “I’ll tackle this another day,” you are not alone.

According to Cindy Scott, a Senior Regional Manager at Charles Schwab, many people do not “have a roadmap for doing anything but earning and spending.” With a lack of general financial education in schools and the (confusing) jargon surrounding topics like owning stocks, trading, and paying off mortgages, the idea of becoming financially literate can seem daunting; however, Scott says that learning about money does not have to be overly complicated.

At its core, financial literacy is the ability to understand money management in order to make productive money decisions.

Each person has different financial resources and circumstances, which means it is essential, regardless of age, that you understand and establish money systems that work for you. This can look like budgeting, participating in low- or no-buy months, and negotiating salaries at your place of work.

Image courtesy of Kailanianna (Kai) Ablog

Addressing the (Green) Elephant in the Room

There is a conversation (or rather, a lack of one) that can contribute immensely to why financial literacy is a skill many people do not have the aforementioned “roadmap” for.

When we were kids, the attitudes those around us held toward money may have influenced our own personal views on finances. Those same perspectives may still inform our approach to money today.

The topic of money can bring up uncomfortable, complicated emotions, especially if we were raised in an environment where money was not as accessible and/or the adults around us taught us little to nothing about money. Some may come from a background or social culture in which sharing financial struggles brought shame to the family; therefore, anything regarding money became taboo.

In her book “Money Out Loud,” Berna Anat mentions that, according to a Cambridge University study, many of us learn most of our money habits by the age of seven.

Unless you received allowance for doing chores or were given cash via birthday cards every year as a child, you may not have had as many chances to hone your ability to hold, budget, and learn about money in an encouraging way.

Our access to financial knowledge may have also been impeded by the obvious absence of financial lessons in school, or due to the fact that many of our parents were working long, hard hours to ensure our family kept a roof over our heads and food on the table. This means that (positive) discussions about money may have been far and few in between. Due to this, we may yearn to “get better” about our money management yet inadvertently feel inadequate, unsure, or doubtful that we could be successful in such an endeavor. We may even avoid it altogether given the sensitivity of the subject matter itself.

The True ‘First Step’ to Learning About Money Starts With You

A step not often talked about when it comes to building financial literacy is learning about our personal “Money Story.”

In short, a Money Story is the personal narrative one has about money; this narrative is influenced and shaped by our experiences growing up, as well as our values and our view of ourselves in the realm of finances.

The discomfort behind the topic of money can stem from our Money Story, where we could have been conditioned to think that an abundance or lack of money was unsafe or shameful; in some cases, money was something that no one talked about. We may have been taught, through the actions of others, that we lacked the capacity to hold money and were influenced to splurge every time we get paid out of fear that we’d never have that same amount again.

Conversely, we may have grown up with the belief that money was always difficult to come by, so every dollar made, after paying for necessities, would be moved into a savings account where it would remain untouched. Although we could have learned that the money would be safely tucked away that way, we often were not taught about other account alternatives, such as a high-yield savings account that could help grow our balance as a result of a higher interest yield rate.

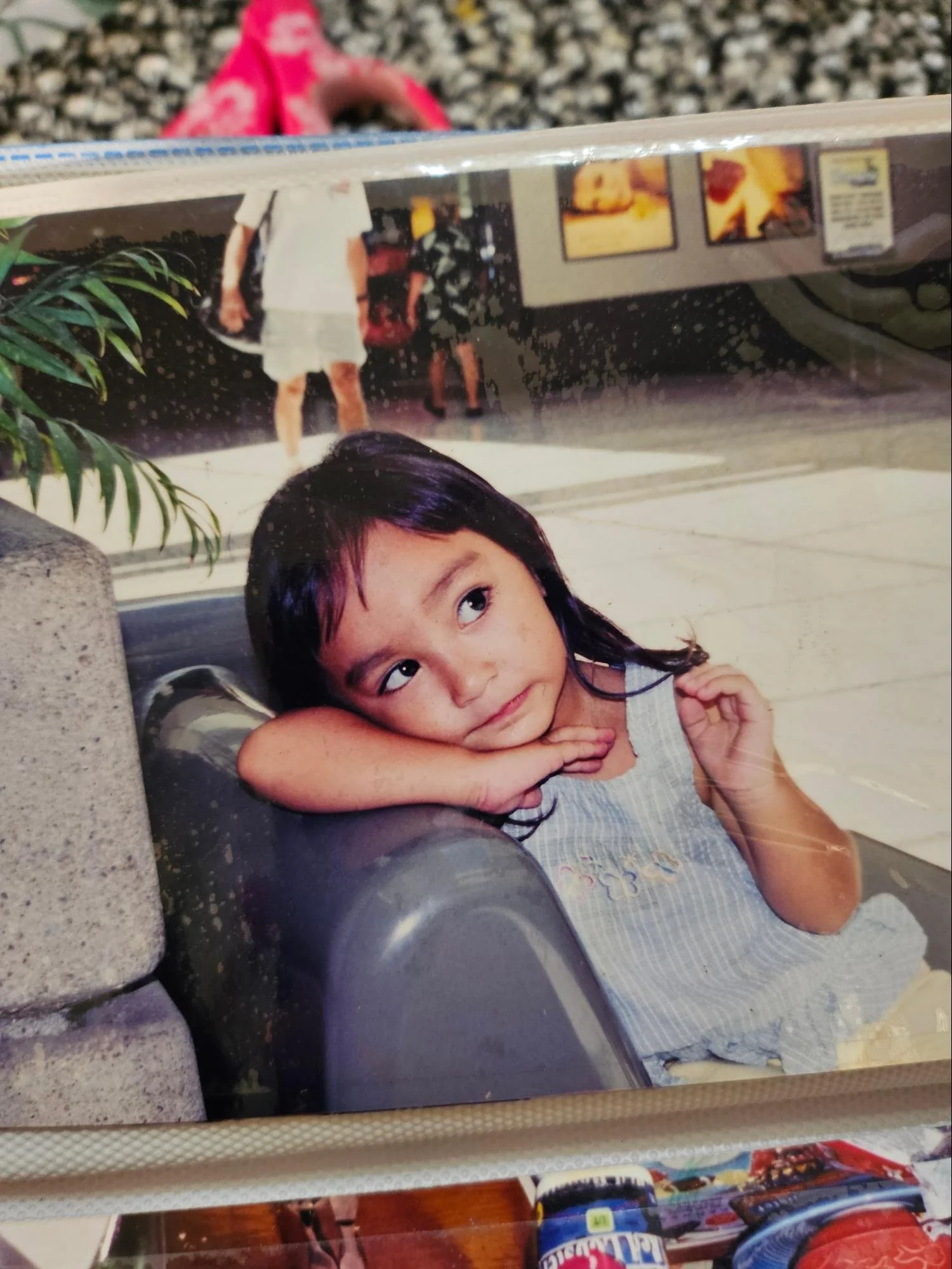

When it comes to Money Stories, I personally experienced both sides of this specific extreme.

I was born to two college-aged parents who had moved from Saipan to Hawaiʻi to pursue higher education; I entered the world during the second semester of their freshman year.

Image courtesy of Kailanianna (Kai) Ablog

Growing up, I was taught to see things as a “Want v.s. Need.” While this was helpful in the long run, as a child, I was conditioned to think that money was scarce and I couldn’t get what I wanted (e.g., the Smucker’s Goober Peanut Butter and Grape Stripes Jar and Scooby-Doo-themed Fruit Snacks). For a large portion of my childhood, I became ashamed to ask for things I wanted because I anticipated the answer would almost always be “No.” When I was given a gift, my follow-up was rarely a “Thank you,” but a “Is this OK (for me to receive this)?”

When I graduated from the University of Hawaiʻi at Mānoa in 2020 and became an independent contractor, I was making more money than I thought I was worthy of making; therefore, when I would get paid, I’d find myself spending my paychecks on clothing, trinkets, and stationery from small businesses.

At the time, I was disheartened that I wouldn’t be able to apply my Anthropology degree in the way I wished to, but knew I wanted to make a difference. So, I tried to spend my money intentionally by “supporting local” during the pandemic.

While I do not regret spending a lot of money in the name of supporting my community, I now recognize a portion of what informed my spending habits was giving my Inner Child what she wanted and also fearing that I wasn’t deserving of the money I made and therefore, lacked the capacity to hold and save it (hence the frequent spending).

Let’s look at another example of a Money Story: You are great at saving money but do so out of fear you won’t have (enough) money in the future; you do not spend money on yourself at all. This could reflect a childhood where no money was used for pleasure, or spending for spending’s sake was looked down upon or seen as selfish.

While our Money Story may be vastly different or shockingly similar to one another’s, we all carry experiences around finances that affect how we see money and how we position ourselves around it.

Leaning into the Discomfort: Understanding Your Money Story

Remembering and processing our Money Story can be very uncomfortable; however, we owe it to ourselves and our personal development to seek silver linings and transmute negative emotions into positive ones, whether it be through harsh lessons or re-framing our experiences in a way to promote growth instead of shame.

If you would like to explore your Money Story, there are many approaches you could take. This includes looking up journal prompts, sitting down with yourself, talking with trusted friends and family, and identifying moments that you viscerally recall where money elicited an emotional response.

If you feel inclined to look into more alternatives, you could also look into Cognitive Behavioral Therapy, which, according to the 2026 American Psychological Association, is a form of psychological treatment that allows a person to recognize the link between “faulty or unhelpful ways of thinking” and “learned patterns of unhelpful behavior” so they may “change their own thinking, problematic emotions, and behavior.”

Becoming aware of the reasoning that informs our actions increases awareness and encouragement in making healthy changes to prevent and/or cease potentially harmful, self-deprecating and self-sabotaging thought patterns and actions. Exploring your Money Story is a vital stepping stone toward achieving more awareness regarding financial literacy because the “root” of many endeavors has to do with our attitude and feelings toward the changes we want to make.

We did not have the ability to choose the financial experiences and perspectives we learned as children; however, as adults, we now have the choice to re-frame our past in a way that propels us toward a more confident, better-informed financial future.